The Three Ghosts of Lifetime Tax Planning: How Advisors Can Solve the Large IRA Tax Problem

High-net-worth clients tend to think their biggest financial issue is market volatility. But that’s not necessarily the case.

Their bigger concern increasingly is the accumulation of future tax liabilities hidden inside oversized portfolios and retirement accounts.

As wealth has grown over the last decade, many affluent households have unintentionally built what Debra Taylor, Managing Partner and Chief Tax Strategist at Carson Wealth, calls “the curse of the large portfolio” — a collection of highly appreciated taxable assets, oversized traditional IRAs, and legacy planning gaps that can quietly erode millions of dollars in after-tax wealth.

For advisors, this creates a major opportunity. Clients need comprehensive lifetime tax planning rather than just investment management.

The Three Ghosts of Lifetime Tax Planning

Taylor’s concept of the “Three Ghosts” is a helpful way to show clients why proactive tax strategy matters long before a tax problem becomes obvious.

The Present Ghost: Why Today’s Low Tax Rates Create Dangerous Complacency

Today’s historically low tax brackets create a false sense of security for many affluent households. Some clients are in what planners often call an “income valley.” They’re earning enough to build wealth, but not yet experiencing the full tax impact of retirement distributions, widowhood, or wealth transfer.

As a result, clients often delay planning because current taxes don’t feel painful. But that’s exactly where advisors can add value.

The best tax planning opportunities often exist before the tax problem arrives.

The Near Future Ghost: Large RMDs and the Widow’s Penalty

The second ghost emerges during retirement.

After decades of maximizing 401(k)s, SEP IRAs, profit-sharing plans, and defined benefit plans, many high-net-worth clients now hold massive traditional IRA balances. What originally looked like smart tax arbitrage can become a long-term tax trap.

Required Minimum Distributions (RMDs) can force retirees into permanently elevated tax brackets, trigger Medicare IRMAA surcharges, increase taxation of Social Security benefits, and reduce deduction eligibility. The problem becomes even more significant after the death of a spouse.

When a surviving spouse moves from Married Filing Jointly to Single filing status, tax brackets compress dramatically while income often remains relatively high. The surviving spouse may simultaneously face:

- Larger RMDs

- Higher effective tax rates

- Reduced deductions

- Higher Medicare premiums

- Lower Social Security income

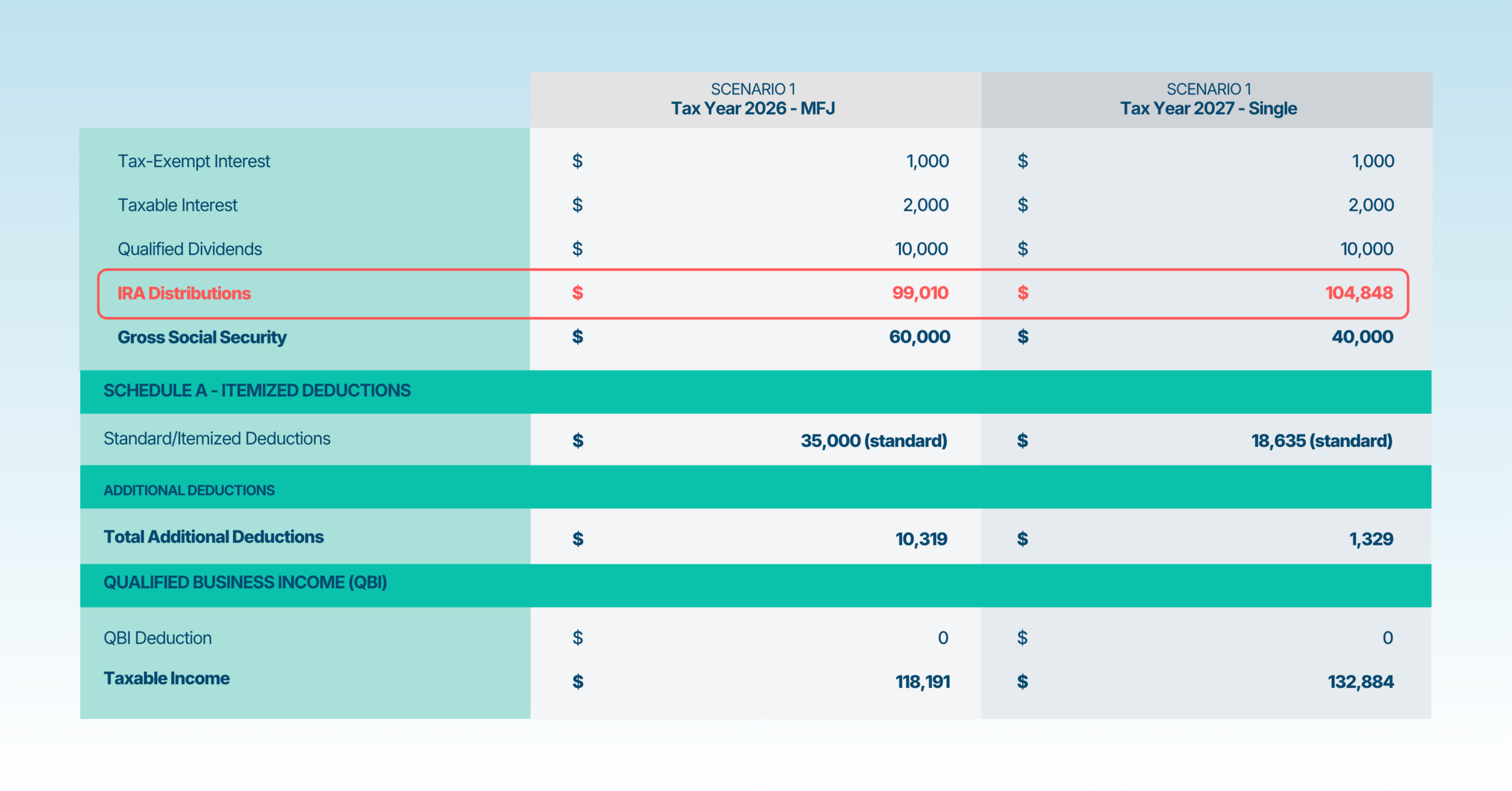

The adjacent Holistiplan charts model the impact of the widow’s penalty on an 80-year-old woman whose husband recently died. She inherits a $2 million traditional IRA but must now file as Single, which reduces her deductions and increases her taxable income.

The financial consequences are serious. The widow’s federal income tax rises by nearly $9,000 while her Social Security benefit drops and her RMD increases by more than $5,000. Her total income has now shrunk by more than $11,000, and it coincides with a significantly larger tax bill.

Taylor said the widow’s penalty demands attention well in advance.

“Almost every time, the widow’s penalty adds another 10% in total tax liability,” she said.

The Future Legacy Ghost: The SECURE Act IRA Tax Bomb

The third ghost is legacy taxation.

The SECURE Act fundamentally changed inherited IRA planning by replacing the lifetime “stretch IRA” with the 10-year distribution rule for most non-spouse beneficiaries. For many affluent families, this creates a multigenerational tax problem.

Adult children often inherit traditional IRAs during their peak earning years. Adding inherited IRA distributions on top of existing income can push beneficiaries into significantly higher tax brackets while also increasing Medicare premiums and other tax-related costs.

In many cases, clients who spent decades deferring taxes are effectively passing a large deferred tax liability directly to their heirs. That’s why, according to Taylor, it requires attention well ahead of time.

“The SECURE Act is an absolute destroyer of family wealth,” she said

The Key Issues of Large Traditional Retirement Accounts

Oversized traditional IRAs have become one of the defining planning challenges for affluent retirees. The core issue is simple: tax-deferred growth eventually creates taxable distribution pressure.

The larger the IRA grows, the larger future RMDs become. And because RMDs are taxed as ordinary income, clients can find themselves trapped in elevated brackets throughout retirement.

This creates several interconnected planning risks:

- Lifetime overpayment of taxes

- Increased IRMAA surcharges

- Tax inefficiency after widowhood

- Heavier tax burdens on heirs

- Reduced flexibility in retirement income planning

Here’s the good news: These issues are often manageable—sometimes avoidable, even—through careful, comprehensive planning.

Potential Solutions for Oversized Traditional IRAs

Asset Location Strategies for Tax-Efficient Retirement Planning

Asset location remains one of the simplest but most underutilized tax-planning tools, Taylor said. She pointed to a use case modeled out through Holistiplan wherein a 40-year-old couple has $250,000 in a traditional IRA and another $250,000 in a Roth IRA.

As is, the couple has a 70/30 bond allocation in both retirement accounts with a blended annual return of 8.5% for each. That results in $2.15 million in pre-tax and $2.15 million in Roth at age 65.

But employing strategic asset location can make a big difference. Moving 100% of bonds ($150,000) and $100,00 of stocks into the traditional IRA and putting 100% of stocks ($250,000) in Roth, the 70/30 allocation remains the same and equals the aggregate risk from the other scenario. And with a blended annual return of 8.5% for both accounts, at age 65 the couple will have $1.6 million in pre-tax and $2.7 million in Roth. That means the couple shifts $550,000 of growth from the traditional IRA to Roth, reducing RMDs throughout their retirement while providing additional tax-free Roth assets.

For advisors, this is an important reminder that tax planning isn’t only about distributions. Portfolio construction decisions matter too. In this example, it literally translated to hundreds of thousands of dollars in tax-free growth.

How Qualified Charitable Distributions (QCDs) Reduce Taxes

QCDs remain one of the most efficient planning tools available for charitably inclined retirees.

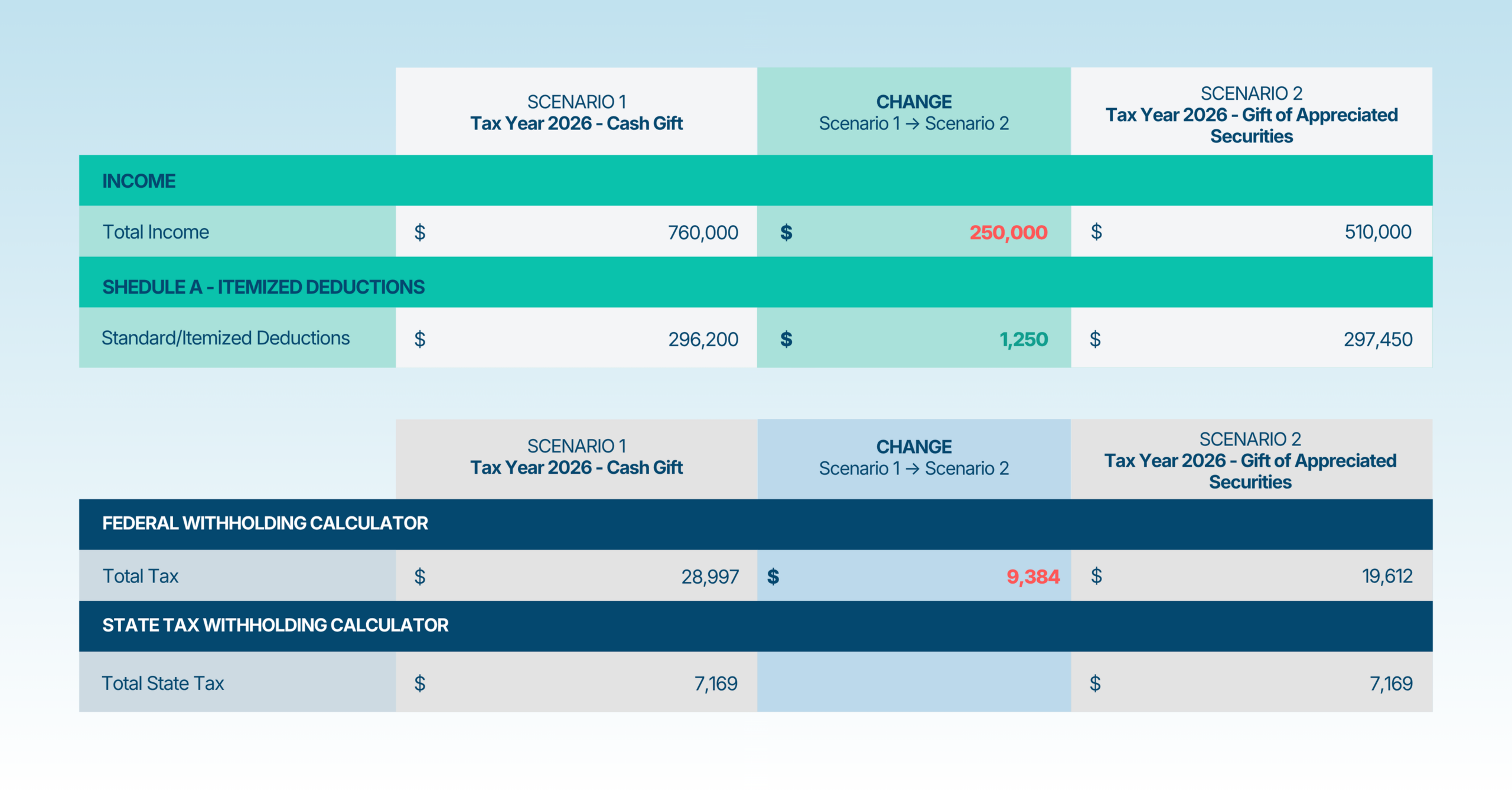

Rather than taking an RMD, recognizing income, and then making a charitable gift, eligible clients can transfer IRA dollars directly to charity. Taylor pointed to another use case modeled through Holistiplan, which you can see in the adjacent charts. In this scenario, a retired couple utilized a $50,000 QCD to save more than $9,000 in federal taxes.

The QCD lowered the couple’s AGI, which can enhance deductions, improve Medicare premium outcomes, and lower taxes on Social Security benefits. Other advantages of such a move include:

- Potentially lower Medicare premiums

- Improved deduction outcomes

- Reduced federal tax liability

For many affluent retirees, QCDs can be much more valuable than traditional charitable deductions.

Strategic IRA Distribution Planning Before RMD Age

Conventional retirement income advice often encourages retirees to spend taxable assets first while allowing IRAs to continue compounding. But that can backfire on affluent households.

Taylor invoked another example modeled through Holistiplan. This one showed how proactively taking $100,000 annually from a traditional IRA before RMD age helped keep a retiree in lower brackets and significantly reduced future RMD pressure.

In this scenario, a 65-year-old single retiree has $2 million in traditional IRA assets and $3 million in taxable assets. By following conventional wisdom and using his taxable assets to cover cash flow needs before beginning RMDs, his IRA continues to grow, leaving him with RMDs between $170,000 and $300,000+ throughout his retirement. That puts him in the 32-35% federal marginal tax bracket.

But by taking the proactive approach and withdrawing distributions of about $100,000 from his traditional IRA every year, the retiree is able to maximize the 22% federal marginal tax bracket while trimming the growth of the retirement account. He continues taking distributions from his taxable portfolio, too, realizing capital gains between $50,000 and $75,000 annually. Altogether, that reduces his IRA balance and lowers his RMD range to $100,000-$200,000 throughout retirement, likely placing him in the 24% federal marginal bracket.

This strategy potentially saves the client hundreds of thousands of dollars. It’s an important reminder that advisors can help clients get the most out of lower tax brackets over time to avoid much larger taxes later.

Roth Conversion Strategies for High-Net-Worth Retirees

Roth conversions remain one of the most powerful long-term tax-planning tools available because they can:

- Reduce future RMDs

- Improve tax diversification

- Protect surviving spouses

- Improve legacy outcomes

- Create tax-free inheritance assets

Taylor cited a Holistiplan model wherein a client converting $400,000 annually for five years created significantly larger after-tax wealth for heirs compared to leaving assets fully inside a traditional IRA. Heirs inheriting a Roth IRA instead of a traditional IRA could potentially avoid millions in taxes under the SECURE Act framework, too.

Roth conversion analysis is highly case-specific. Advisors must evaluate:

- Current versus future tax rates

- State tax considerations

- IRMAA exposure

- Estate objectives

- Time horizon

- Cash available to pay taxes

- Beneficiary tax situations

But the broader point remains: large traditional IRAs should rarely be left unmanaged.

Why Coordinated Tax Planning Is the Future of Wealth Management

The main thing about lifetime tax planning, Taylor said, is that affluent clients increasingly need coordinated advice across three major planning lanes:

- Investment management

- Retirement and financial planning

- Tax and estate planning

Commonly, such clients don’t have someone coordinating that full picture, with their advisory services scattered. Their CPA focuses on compliance. Their investment advisor focuses on portfolio performance. Their estate attorney focuses on documents.

Major tax opportunities are falling between the gaps.

And that’s where you can differentiate yourself with truly comprehensive planning. Leverage Holistiplan to uncover planning opportunities that your competitors are missing—the kind of opportunities that save your clients hundreds of thousands of dollars. You’ll be able to deliver in-depth analysis in mere minutes without having to add staff.

Holistiplan simplifies tax planning for advisors by synthesizing clients’ financial documents to identify where and how their money could grow with Roth conversions, strategic withdrawals, charitable giving, and more.

Taylor said it’s the only way to provide your clients with the comprehensive tax planning they’re looking for.

“You must use this software to model out all these types of permutations so that you can be delivering to the client the level of services that they need and so that you can save them literally millions of dollars in taxes,” she said.